19 April 2026

Global smartphone shipments fell 6% year-over-year in Q1 2026, according to preliminary estimates from Counterpoint Research’s Global Smartphone Market Monitor. The primary culprit: a shortage of DRAM and NAND memory components that has compressed OEM margins, disrupted production schedules, and pushed manufacturers to delay launches and cut lower-margin models.

Consumer sentiment compounded the supply-side pressure. Economic uncertainty tied to Middle East tensions kept discretionary spending cautious, even as some OEMs frontloaded shipments to get ahead of anticipated component price hikes and rising logistics costs — partially offsetting what could have been a steeper decline.

The pressure is not distributed evenly. Premium brands are weathering the storm. Volume-driven players are struggling. And in the secondary market, the conditions are creating a distinct opportunity — one that businesses sourcing wholesale refurbished iPhones or working as a refurbished Samsung wholesale supplier are well placed to capture. Here is what the data shows.

Why Shipments Are Falling: Memory Players Prioritize AI Over Smartphones

The memory shortage gripping the smartphone market is not a simple supply chain disruption — it is the result of a deliberate reallocation of production capacity. Memory manufacturers are prioritizing AI data center demand over consumer electronics, leaving smartphone OEMs with constrained supply and little pricing power.

The knock-on effects are significant: higher Bills of Material (BOM) costs are being passed directly to consumers, launch timelines are being extended, and brands are rationalizing their portfolios to cut products that can no longer be made profitably at competitive price points. According to Counterpoint Research, the memory crunch is expected to persist until late 2027 — making this a structural challenge, not a temporary dip.

Rising energy prices and higher logistics costs are adding further pressure on top of the component shortage, keeping the overall cost environment elevated across the supply chain.

Apple Leads a Q1 for the First Time — Here Is Why

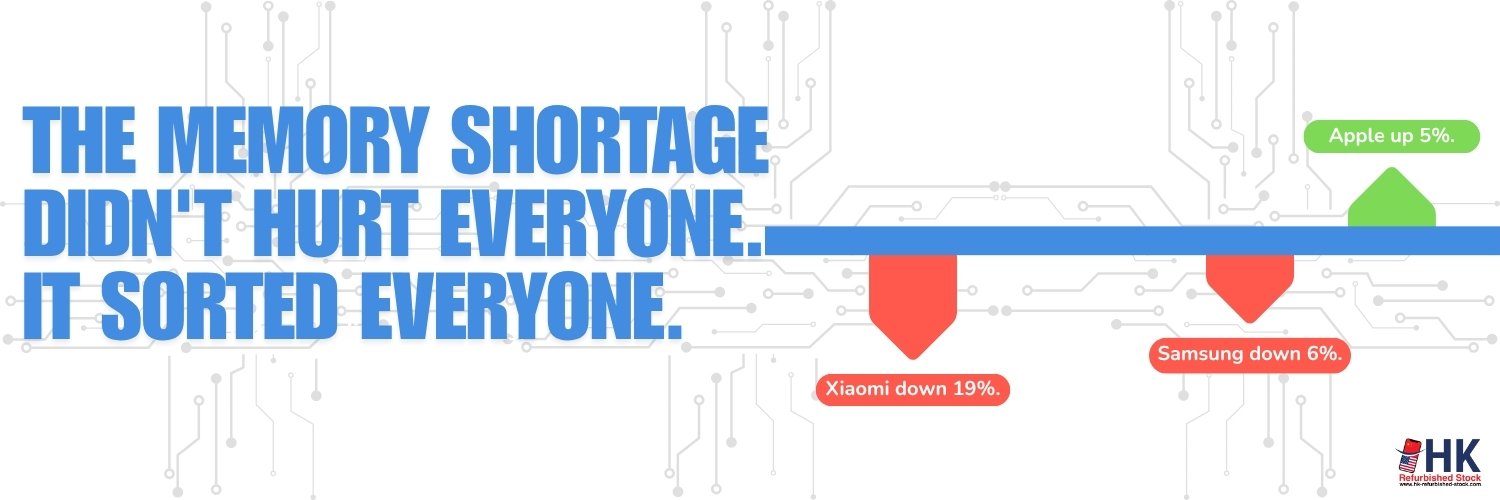

Apple captured 21% of global smartphone shipments in Q1 2026, growing 5% year-over-year and claiming the top position in a Q1 period for the first time. Several factors converged to make this possible.

- Supply chain resilience: Apple’s highly integrated supply chain makes it the most insulated major brand against the memory crisis. By securing component commitments early and managing its production ecosystem tightly, Apple maintained availability when competitors were constrained.

- iPhone 17 demand: Continuous strong demand for the iPhone 17 series sustained volume growth despite a softer macroeconomic backdrop.

- Trade-in programs and ecosystem stickiness: Aggressive trade-in programs made upgrading more accessible, while Apple’s broader ecosystem kept existing users within the brand.

- Asia-Pacific momentum: Apple achieved notably stronger growth in China, India and Japan — three of the highest-potential smartphone markets globally.

For the secondary market, Apple’s strong trade-in activity has a direct consequence: higher volumes of prior-generation iPhones flowing back into the supply chain. If you are looking to build out your refurbished iPhone inventory ahead of rising demand, explore our wholesale refurbished iPhone stock.

Samsung: A Delayed Launch Masks Underlying Demand

Samsung recorded a 6% year-over-year shipment decline in Q1 2026, finishing with a 20% market share. Two factors drove this: weakness in the mass-market and entry-tier segment — where memory cost pressures hit hardest — and the delayed launch of the Galaxy S26 series, which pushed anticipated Q1 volume into later quarters.

The delay should not be mistaken for weakening demand. When the S26 did launch, early momentum was strong — with the Ultra variant seeing the highest traction, consistent with the broader premiumization trend across the market. To manage rising cost pressures, Samsung has adjusted its portfolio strategy: streamlining entry-level options, emphasizing higher-tier configurations, and effectively raising starting prices while reinforcing its premium positioning.

For wholesalers, Samsung’s deliberate shift toward premium is a useful signal. Demand for refurbished Galaxy S-series models — and Ultra variants in particular — is likely to strengthen as upgrade cycles from the S26 generation play out. View our current refurbished Samsung wholesale inventory to plan your stock accordingly.

The Rest of the Market: Sharp Divergence Below the Top Two

Xiaomi: Volume Under Pressure

Xiaomi held its third-place position with a 12% global market share, but recorded the steepest decline among the top five brands — down 19% year-over-year. Its heavy exposure to the entry-level segment makes it particularly vulnerable to rising memory costs, and the brand is now streamlining its product lines and refocusing on core regions while trying to gain traction in the premium segment with the Xiaomi 17 series in China.

OPPO and vivo: Holding Ground

OPPO and vivo captured fourth and fifth place with 11% and 8% market share respectively, each declining a marginal 2% year-over-year. vivo retained its market leadership in India by leveraging its mid-range lineup for high-value upgrades. OPPO saw strong performance in the entry-level segment with its A5 series, while its ultra-flagship Find N5 was well received at the premium end.

Standout Performers: HONOR, Google, and Nothing

While most of the market contracted, three brands bucked the trend. HONOR and Nothing each grew 25% year-over-year, while Google’s Pixel lineup grew 14%. HONOR’s growth was driven by overseas expansion and a regionally tailored portfolio backed by aggressive promotions. Google continued to strengthen its presence in mature markets on the back of its edge AI capabilities, computational photography, and clean software experience. Nothing, meanwhile, continues to benefit from its distinctive design and niche positioning — its recently launched Phone (4a) drove strong consumer response and accelerated the brand’s growth further.

The Refurbished Market: A Direct Beneficiary of the Memory Crunch

One of the clearer structural outcomes of the memory shortage is an acceleration of demand for refurbished devices. As new device prices rise in response to higher BOM costs, a growing share of budget-conscious consumers — particularly in price-sensitive regions — are turning to the secondary market for quality devices at accessible price points.

Counterpoint Research explicitly notes that OEMs are expected to leverage refurbished devices as a tool to retain budget users as the memory crunch persists through 2026 and potentially into 2027. This is not a short-term shift — it reflects a structural reorientation of how the market serves cost-conscious consumers.

For wholesalers and resellers, the implication is clear: positioning now — with the right inventory of quality refurbished iPhones and Samsung devices — puts you ahead of demand that is only expected to grow. At HK Refurbished Stock, we work with partners to ensure they have the stock they need, when they need it.

Outlook: What to Expect Through 2026 and Beyond

The overall market outlook for 2026 remains cautious. The memory crunch is not expected to resolve quickly — Counterpoint Research’s preliminary view points to continued constraints potentially lasting until late 2027. In response, OEMs are expected to prioritize value over volume, cut low-margin models, and lean further into software, ecosystem expansion, and services as primary growth levers.

Premiumization will continue to hold steady, but margin pressure will intensify across the board. Brands without the supply chain integration of Apple or the scale of Samsung will face increasingly difficult trade-offs.

For the secondary market, this environment represents a sustained tailwind. Rising new device prices, extended upgrade cycles, and growing institutional recognition of refurbished as a viable channel all point in the same direction.

Key Takeaways

- Global smartphone shipments declined 6% YoY in Q1 2026, driven by DRAM and NAND memory shortages.

- Apple led Q1 for the first time with 21% market share and 5% YoY growth, underpinned by supply chain resilience and iPhone 17 demand.

- Samsung declined 6% YoY to 20% share, largely due to delayed S26 launch and entry-tier weakness — not a loss of demand.

- Xiaomi fell 19% YoY — the steepest top-five decline — due to heavy exposure to the memory-impacted entry segment.

- HONOR, Google, and Nothing bucked the trend, growing 25%, 14%, and 25% YoY respectively.

- The memory crunch may persist until late 2027, making the refurbished market a structural beneficiary of rising new device prices.

Position Your Inventory Ahead of the Demand Shift

With new device prices rising and the memory crunch set to last into 2027, demand for quality refurbished devices is only heading in one direction. Whether you are stocking refurbished iPhones, refurbished Samsung devices, or building a broader secondary market portfolio, HK Refurbished Stock can help you source the right models at the right time.

Get in touch with our team to discuss stock availability, pricing, or to request a wholesale quote.