06 May 2026

Samsung Electronics reported first-quarter 2026 net profit of more than $30 billion — not only its highest-ever quarterly result, but a figure that nearly matched its previous record for a full year. Around 94% of that operating profit came from semiconductors. The driver: an AI-fueled memory chip boom that has pushed DRAM and NAND flash prices to historic levels and elevated Samsung, SK Hynix, and Micron Technology into a new tier of global corporate profitability.

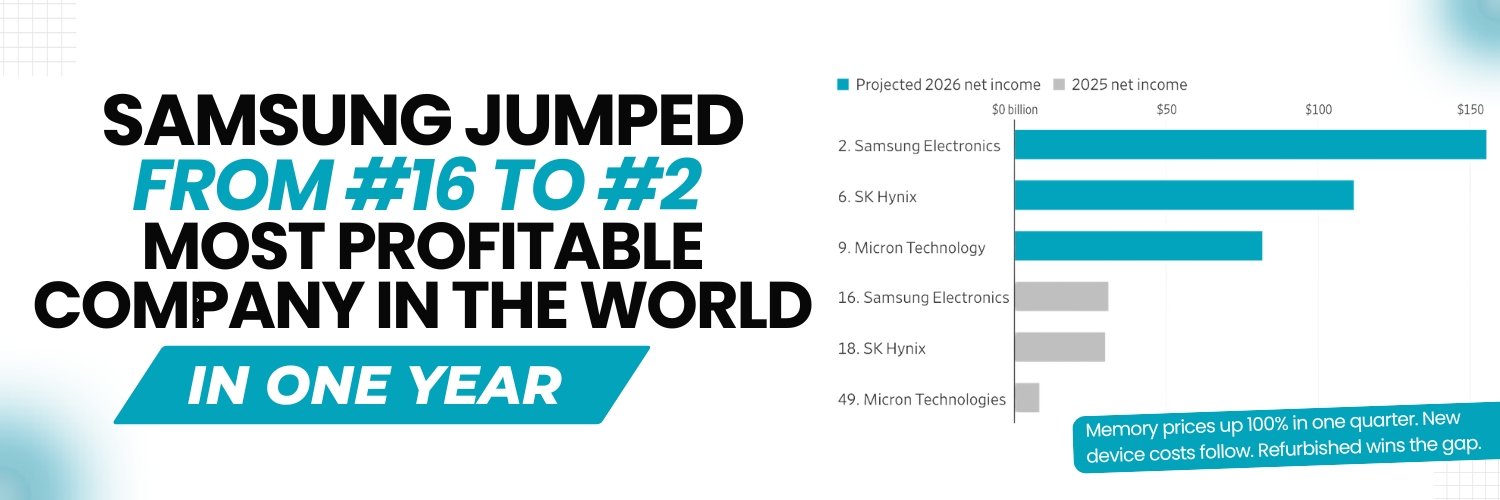

According to FactSet estimates, the three memory giants are collectively projected to generate around $350 billion in net profit for 2026. Samsung is expected to vault from 16th to 2nd place on the global net income rankings — surpassing Alphabet, Microsoft, and Apple. SK Hynix is projected to rise from 18th to 6th, and Micron from 49th to 9th. A year ago, none of the three cracked the top 10.

For businesses operating in the secondary smartphone market — whether you source refurbished Samsung phones wholesale or wholesale refurbished iPhones — the memory shortage is not just a headline. It is the structural force driving up new device prices, tightening supply, and pushing more consumers toward refurbished alternatives. At HK Refurbished Stock, we track these dynamics to help our partners stay ahead.

How AI Created the Most Severe Memory Shortage the Market Has Ever Seen

The memory crunch has its roots in a production capacity decision made over the past several years. Memory manufacturers shifted production toward high-bandwidth memory (HBM) — a specialized form of DRAM that is stacked in layers and packaged alongside Nvidia’s GPU chips to accelerate AI computing. Training large language models requires pairing Nvidia processors with HBM, and as AI investment surged, so did demand for this specialized chip type.

The consequence: production capacity for conventional DRAM and NAND flash — the memory used in smartphones, PCs, and general servers — was constrained. Supply fell short of demand. Prices rose sharply.

More recently, demand has risen for AI inference — the computing that allows trained AI models to respond to user queries in real time. Inference requires general servers, which use conventional memory. That development has elevated demand for the same chips that power smartphones and PCs, compounding the shortage further.

The result is what Marcus Chen, executive vice president at FusionWorldwide, described as the most severe memory shortage the market has ever seen. Most of the customers Chen’s firm supports are receiving only 30% to 50% of the memory chips they need. Some are receiving even less.

Memory Prices Have Nearly Doubled — And the Shortage Is Getting Worse

Memory prices in Q1 2026 grew nearly 100% from the prior quarter — roughly double the growth that analysts had initially projected, according to TrendForce. Operating profit margins for both DRAM and NAND flash have approximately doubled from their usual levels, reaching around 80% for DRAM and up to 60% for NAND flash, according to MS Hwang, a semiconductor research analyst at Counterpoint Research.

The supply crunch is not expected to ease quickly. New chip-making facilities (fabs) cost upward of $20 billion each and take years to build. Samsung, SK Hynix, and Micron are all constructing new capacity, but production is unlikely to reach full levels until late 2027 or 2028. Based on Samsung’s prebooked orders, Jaejune Kim, the company’s executive vice president for memory, stated on an earnings call that the supply crunch is expected to grow worse next year. Available supply, he said, is far short of customer demand.

Adding further pressure: large companies in the server, PC, and smartphone businesses are paying premiums to secure larger volumes of memory, effectively constraining supply for rivals. As Hwang put it, the underlying dynamic is that whoever dominates memory supply can dominate AI — an incentive that is driving aggressive stockpiling behavior across the industry.

Samsung’s Position: Dominant in Memory, Squeezed in Smartphones

Semiconductor Profits at Record Levels

Samsung holds a 36% share of the global DRAM market and a 28% share of NAND flash, making it the largest player in both segments. With memory prices nearly doubling in Q1 2026 and profit margins hitting record levels, Samsung’s semiconductor division is generating earnings at a scale the company has never previously achieved. Since the start of 2026, Samsung’s shares have risen 72%.

The Smartphone Side: A Different Story

Samsung’s semiconductor boom stands in contrast to its smartphone division, which has faced a more difficult 2026. Cumulative smartphone shipments declined 6% year-over-year through Week 13, driven by the delayed Galaxy S26 launch and weakness in the entry-tier segment — where memory cost increases have hit hardest. The Galaxy S26 launch in March reversed the trajectory, with early sales running 4% ahead of the S25 launch period and 29% higher year-over-year in the US specifically.

For refurbished market participants, Samsung’s smartphone trajectory has a direct read-through: the S26’s strong launch is accelerating trade-in activity, expanding the pool of prior-generation Galaxy devices entering the secondary market. Explore our refurbished Samsung wholesale inventory to plan your sourcing strategy.

SK Hynix and Micron: The Other Memory Beneficiaries

SK Hynix — which holds a 32% share of the DRAM market and a 22% share of NAND flash — is projected to rise from 18th to 6th place in global net income rankings for 2026, with estimated annual net profit of around $112 billion. Its shares have risen 90% since the start of the year.

Micron Technology, which holds a 22% DRAM share and 13% NAND flash share, is projected to jump from 49th to 9th place globally, with estimated annual net profit of around $82 billion — up from $8.5 billion in 2025. Micron’s shares have gained 65% since January.

Together, these three firms dominate global memory production and are all navigating the same fundamental tension: building new capacity as fast as possible while the current shortage generates extraordinary returns.

What the Memory Boom Means for Refurbished Smartphone Resellers

New Device Prices Are Rising — Refurbished Becomes More Compelling

The memory shortage is pushing up the cost of new smartphones across all segments. As OEMs pass higher BOM costs on to consumers, the price gap between new and refurbished devices widens — making refurbished alternatives more attractive to a broader segment of buyers. This dynamic is already visible in market data: Counterpoint Research projects global refurbished smartphone market growth of around 11% in 2026, with LATAM outpacing that at 12%.

The Shortage Is Structural — It Won’t Resolve Quickly

New fab construction timelines mean the memory shortage is unlikely to meaningfully ease before late 2027 at the earliest. For refurbished resellers, this is a multi-year tailwind, not a short-term opportunity. Businesses that build out their refurbished inventory now — particularly in high-demand segments like premium iPhones and Galaxy S-series devices — are positioning ahead of a demand shift that has structural momentum behind it.

Supply Chain Contracts Are Getting Longer — Secure Your Sources Early

The memory market is seeing a shift from informal handshake deals to binding long-term contracts, with some running as long as five years and requiring upfront prepayments of around 30% of costs, according to Citi semiconductor analyst Peter Lee. While this applies primarily to chip manufacturers and their direct customers, the principle translates to the refurbished supply chain: businesses that establish reliable sourcing relationships now will be better insulated from availability and pricing volatility. HK Refurbished Stock works with wholesale partners to provide consistent supply of quality refurbished devices — reach out to discuss your sourcing needs.

Key Takeaways

- Samsung reported Q1 2026 net profit of more than $30 billion — a quarterly record — with 94% coming from semiconductors.

- Samsung, SK Hynix, and Micron are projected to collectively generate ~$350 billion in net profit for 2026, all entering the global top-10 profit rankings for the first time.

- Memory prices rose nearly 100% in Q1 2026 vs. the prior quarter — roughly double initial projections.

- DRAM operating margins have reached ~80%; NAND flash margins up to ~60% — roughly double their usual levels.

- Most customers are receiving only 30%–50% of the memory chips they need; the shortage is expected to worsen in 2027.

- New fab capacity won’t hit full production until late 2027 or 2028, making this a structural — not cyclical — shortage.

- Rising new device prices are a structural tailwind for the refurbished smartphone market through at least 2027.

Position Your Inventory Ahead of a Multi-Year Demand Shift

The memory shortage is not resolving soon — and rising new device prices mean refurbished demand will keep growing. Whether you’re building out your refurbished Samsung wholesale stock, sourcing wholesale refurbished iPhones, or expanding your secondary market portfolio, HK Refurbished Stock can help you source the right devices at the right time.

Contact our team to discuss availability, grades, and wholesale pricing.